2. Investment funds and asset management landscape

Introduction

The asset management and funds sector is about investing the savings of different types of customers through a variety of legal structures, frameworks and products into investments, whether they be public or private or different asset classes. The sector is diverse, comprises both regulated and unregulated activity and is characterised by a number of different participants.

The funds and asset management industry has grown in size and scale over recent decades as savings have grown, funds have moved into new areas of activity and investors have become increasingly active. Also contributing to this growth is the fact that asset values have generally risen, defined benefit pension provision has reduced and globalisation has facilitated the sector’s international and cross-border footprint.

Over several decades, Ireland’s regulatory and statutory regimes have developed to address the needs of the sector. Ireland offers a range of fund structures that can be tailored to suit investors with diverse investment objectives while the regulatory and supervisory focus has evolved in tandem with the sector and in response to regulatory requirements developed at EU level.

Consequently, Ireland has become a centre of excellence for investment funds and a location of choice for specific investment fund types. Due to the depth of expertise and the experience established in the Irish funds eco-system, Ireland is currently the second largest fund domicile in the EU. It is the EU's leading location for Exchange Traded Funds (ETFs) and one of the largest domiciles for Money Market Funds (MMFs). Ireland is also recognised as one of the key global hubs for fund service providers supporting investment funds established in Ireland, the EU or other international jurisdictions.

Ireland also has a significant amount of other non-bank financial intermediation activity such as securitisations (which use “Special Purpose Entities” or SPEs). Financial services associated with the use of SPEs are significant and there are a range of firms involved in servicing them.

Relevant Terms of Reference

- Assess how the funds sector has evolved since policy supports to attract international financial services activity to Ireland began in the late 1980s

- Outline the current landscape of the asset management and funds servicing, having regard to domestic and international debates on the role of the non-bank sector

Historic context

The genesis of Ireland’s modern financial services sector was brought about due to a confluence of factors. Ireland joined the European Economic Community (EEC) in 1973. By 1985, it had become a major destination for foreign direct investment (FDI), building on its advantages of the English language, common law, location between the USA and UK, long list of double tax treaties and access to markets enabled by the EEC. In the following year, the Finance Act 1986 put in place the policies to support private sector investment in the Dublin’s docklands area. The Finance Act 1987 built upon this premise by allowing for a specific 10 per cent corporation tax rate for companies operating in a special economic zone in the soon to be developed International Financial Services Centre (IFSC). This 10 per cent taxation regime for “designated financial services activities” in the IFSC was replaced ahead of its expiration by a national corporate tax rate of 12.5 per cent, which came into effect in 2003. The success of the 10 per cent corporation tax rate in establishing of Ireland as a centre for international financial services was also evidenced in the Shannon region which led to Ireland becoming an important centre for aircraft leasing.

Also key to the early growth of Ireland as a fund domicile was the quick implementation of the 1985 UCITS (undertakings for collective investment in transferable securities) Directive. Prior to 1985, cross-border asset management in Europe was a relatively small industry, focusing mainly on private wealth management, with London, Switzerland and Luxembourg as its key centres. By facilitating collective investments in securities, the 1985 UCITS Directive stimulated the growth of funds and laid the foundations for an integrated market for the production and distribution of fund services. The Directive meant that new investment funds could be registered in, and existing investment funds relocated to, EU Member States that were not the main markets for the distribution of these funds. Luxembourg was the first country to implement the Directive in 1988. Ireland followed in 1989, with the first Irish UCITS launched in the same year.

At a national level, legislation was drafted to expand the range of investment fund structures that could be domiciled in Ireland. This included a new Companies Act and the Unit Trust Act in 1990, later followed by the introduction of an Investment Limited Partnership in 1994 (subsequently amended in 2020), the Investment Funds, Companies and Miscellaneous Provisions Act 2005 which established the Common Contractual Fund and, more recently, the creation of the Irish Collective Asset Vehicle (ICAV) structure in 2015.

Several factors can explain the fast growth of Ireland as a fund domicile since the early 2000s. The creation of the Eurozone accelerated the integration of the funds industry and made the Eurozone a more attractive place for investments. Further changes to regulation also fuelled integration, principally the fourth UCITS Directive (UCITS IV Directive) which introduced a ‘passporting’ framework that allowed products and services approved in one Member State to be recognised in other Member States without additional approvals being required. Implemented in 2011, the UCITS IV Directive lifted the requirement for fund management companies to be domiciled in the same country where the fund is domiciled. This aided the growth of certain EU Member States, including Ireland, as both domiciles for the administration of fund structures and locations to which the investment decisions can be delegated.

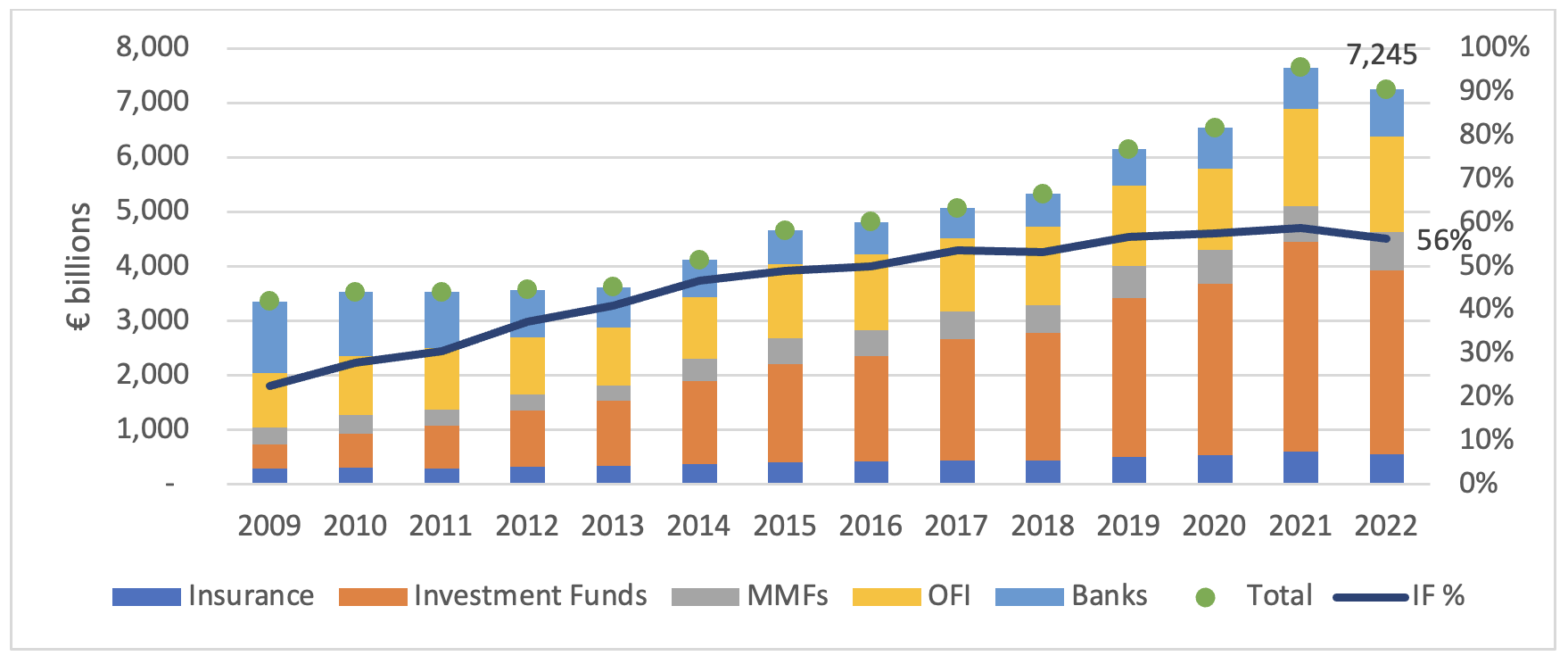

The investment funds sector is now a significant part of a growing financial sector in Ireland, accounting for 56 per cent of assets at the end of 2022, as detailed in Chart 1.

|

Chart 1. Growth of Regulated Financial Sector Assets in Ireland |

|

|

Source: Central Bank of Ireland |

Ireland’s funds sector is large relative to other European countries, being the 2nd largest domicile for regulated funds - UCITS and alternative investment funds (AIFs) - in the EU, as detailed in Chart 2.

|

Chart 2. Ireland as a Domicile Compared to Selected European Countries |

|

|

Source: EFAMA |

Recent trends

Changes in the structures and activities of fund management companies have recently been evident in Ireland. These include consolidation and moves towards providing a broader range of services such as individual portfolio management, risk management and fund administration services, particularly on a third party basis. There have also been significant regulatory developments including the provision of additional guidance in relation to substance requirements and governance enhancements which have led to the reduction in Self-Managed Investment Companies (SMICs) and the increase in third party management companies. There has been notable growth in Irish fund management companies providing discretionary portfolio management and other non-core service services. In 2019, there was approximately €19 billion in assets under management (AUM) for such services. By 2022, this figure had increased to €432 billion. There is also increasing growth and concentration in third party fund managers with AUM reaching nearly €540 billion.[1]

Future outlook

Changing investor demographics and demands, technological innovation, including from automation and tokenisation, and new types of investment products such as ESG (environmental, social and governance) related products will shape the development of the funds sector, its activities and products, in the years to come.

The sector will continue to grow in size and importance, particularly as an alternative source of financing for the real economy, and the nature of activities undertaken in the sector will also evolve and expand. These inherent characteristics can give rise to new types of risks and opportunities.

The regulatory environment will continue to adapt and develop in response to market developments, particularly in the areas of investor protection, financial stability, sustainable finance, technology, innovation and digital assets. There will also be future changes to the European frameworks under the Capital Markets Union (CMU), including the Retail Investment Strategy, ongoing review of files and in the context of the broader discussion of open strategic autonomy in Europe.

Key elements of the funds and asset management sector

Broadly speaking, there are two main elements to consider when examining investment funds and asset management. The first is the fund product, that is, the investment funds which are established. The text below sets out to examine investment funds under the subheadings of fund categories, fund products and asset classes. The second element of the industry that is particularly important to Ireland relates to the servicing of investment funds.

Funds may be domiciled in Ireland or non-domiciled. Irish-domiciled investment funds are established under the applicable domestic legislation. Non-domiciled funds are established, authorised and regulated/supervised in a jurisdiction other than Ireland. However, the existence of harmonised European frameworks allow Irish-domiciled funds (UCITs and AIFs) to be passported across the EU without restrictions.

I. FUND CATEGORIES

Investment funds are established for the purpose of investing the pooled funds of investors (held as units or shares) in assets in accordance with investment objectives and investment policies published in a prospectus.

The regulated fund sector, made up of Irish resident UCITS and AIFs, has grown significantly in recent years.[2] There are also sub-sets of these funds which are subject to specialist fund regulations. These can include MMFs, European Long-Term Investment Funds (ELTIF), European Sustainable Entrepreneurship Funds (EuSEF) and European Venture Capital Funds (EuVECA).

|

UNDERTAKINGS FOR THE COLLECTIVE INVESTMENT IN TRANSFERABLE SECURITIES UCITS are investment funds that can be established under a European regulatory framework designed for the protection of retail investors. The UCITS Directive has two main areas of focus:

UCITS established in one EU Member State have the benefit of being capable of being sold in another EU Member State. UCITS funds are a highly popular form of investment globally and especially for European retail investors. The UCITS framework has been in operation since 1988. |

|

ALTERNATIVE INVESTMENT FUNDS AIFs are investment funds established by Alternative Investment Fund Managers (AIFMs). AIFMs have been authorised since 2011. AIFs are intended for investment mainly by professional investors though they may be marketed to retail investors. They are authorised by the Central Bank in one of two categories:

The AIFM Directive (AIFMD) provides for detailed conduct and operational rules in relation to AIFMs. It does not establish rules in relation to AIFs themselves and so AIFs may invest in a wide array of assets (which may or may not be liquid) and may provide for different frequencies at which investors can redeem from the AIF (indeed some AIFs may permit no opportunity for an investor to request a redemption). Where AIFs are regulated, rules in relation to permissible assets for investment, investment borrowing and leverage limits are provided for by the Central Bank. While AIFs may be established in one EU country and be sold in another, the process is different to that for UCITS. |

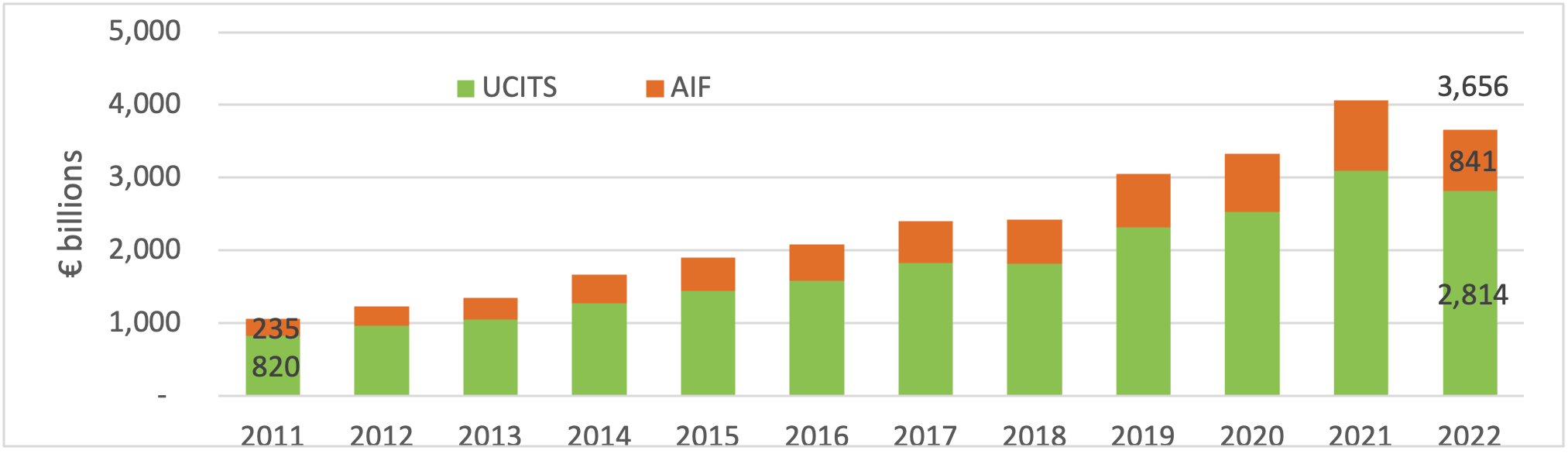

The assets under management in regulated structures in Ireland have grown strongly, reaching €3.65 trillion at the end of 2022.

|

Chart 3. Growth of Regulated Funds Structures in Ireland (AUM) |

|

|

Source: EFAMA |

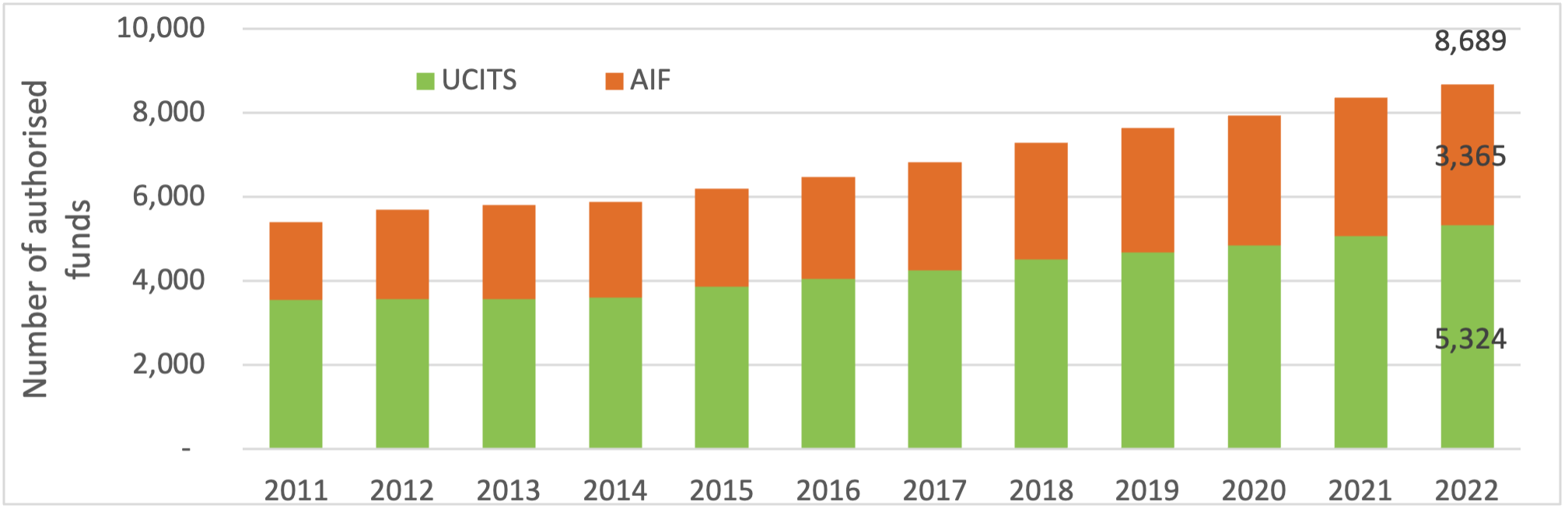

The number of regulated structures in Ireland had increased to 8,689 by the end of 2022.

|

Chart 4. Growth of Regulated Funds Structures in Ireland (Number of Funds) |

|

Source: EFAMA |

European Long Term Investment Funds (ELTIF)

The ELTIF Regulation establishes a pan-European regime for AIFs which aims to channel the capital they raise towards long-term investments in the real economy. The ELTIF regulatory framework sets out detailed fund rules on eligible assets and investments, diversification and portfolio composition, leverage limits and marketing. However, since the adoption of the Regulation in 2015, the market for ELTIFs has been relatively limited. No ELTIFs have been launched in Ireland, though Luxembourg, France, Italy and Spain have authorised 89 collectively.

|

Chart 5. Authorised ELTIFs as at 12 June 2023 |

|

|

Source: ESMA[3] |

As part of its CMU package presented in November 2021, the Commission proposed a targeted review of the ELTIF Regulation to improve the functioning of the regime. The revised ELTIF Regulation, which is intended to make the ELTIF more flexible in terms of its investment rules and encourage greater participation by retail investors, entered into force in April 2023 and will apply from January 2024.[4]

II. FUND PRODUCTS

Two types of investment funds are particularly prominent in Ireland: Exchange Traded Funds (ETF) and Money Market Funds (MMF).

Exchange Traded Funds

An ETF is a collective investment scheme that is actively traded on a stock exchange or other trading venue. It is often described as having “hybrid” features because it is an open-ended investment fund and its shares are also actively traded. A key advantage for a retail investor is that they are usually not overly exposed to a single asset and, therefore, the performance of a single company or market. From a European perspective, an ETF may be established as a UCITS or as an AIF. However, with limited exceptions, ETFs are authorised by the Central Bank of Ireland under the UCITS Directive.

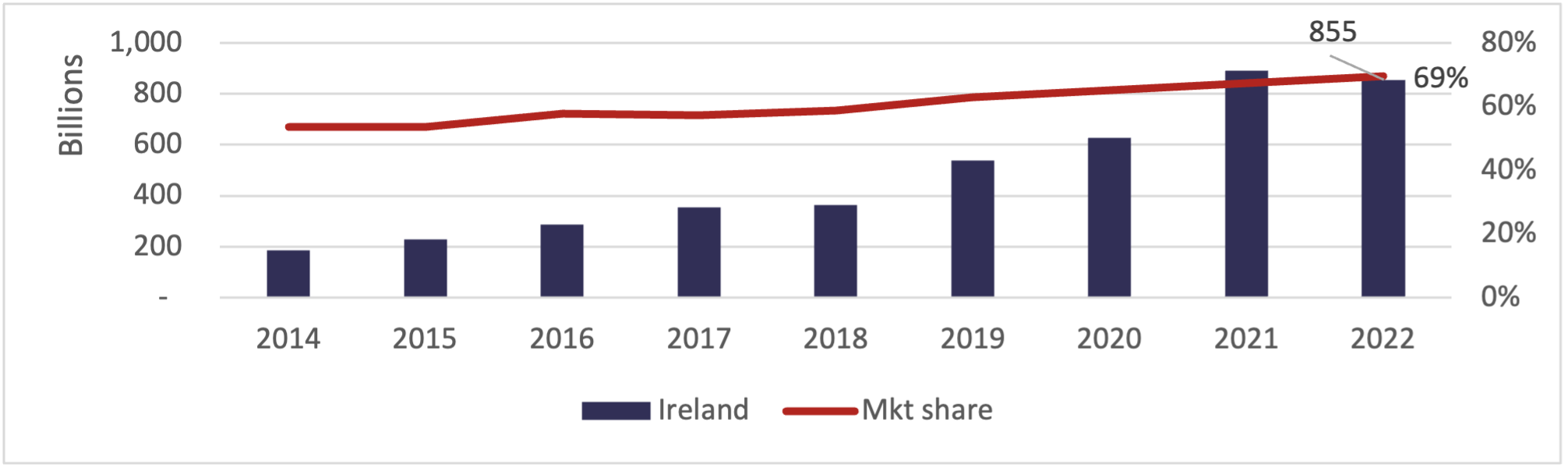

ETFs have experienced exponential growth since they were first established in 1990. The ETF market is significant in size and has grown at a rapid pace over recent years. Since the launch of the first European ETF in 2000, Ireland has become a centre of excellence in supporting the operational aspects of ETFs. This includes the development of a large pool of expertise and experience across a range of essential services from fund administration, legal, tax, accounting, audit and depositary services. As a result, Ireland has become the number one European domicile for ETFs, with many of the largest global ETF promoters choosing to domicile their European products in Ireland. By the end of 2022, over 1,300 ETFs were domiciled in Ireland, amounting to €855 billion AUM (69 per cent of the total ETF AUM in the EU) and accounting for over 20 per cent of the funds domiciled in Ireland.[5]

|

Chart 6. Growth of ETFs in Ireland |

|

|

Source: ECB |

Money Market Funds

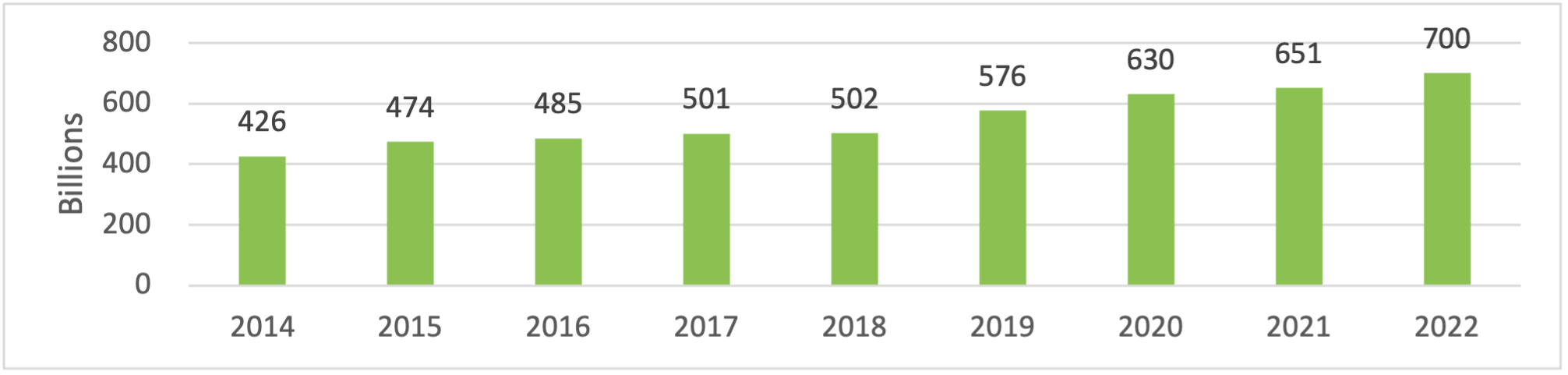

MMFs generally invest in short term deposits and debt instruments and they perform an important role for many different types of investors, including as a cash management and liquidity tool. MMFs can be established in Ireland as either UCITS or AIFs, although, in practice the vast majority of MMFs are UCITS funds. MMFs form a large and important sector in the European and global investment fund landscape. Ireland is the premier location in Europe for establishing and servicing MMFs and is domicile to €700 billion of MMFs, roughly 45 per cent of MMFs in the EU. The majority of MMFs domiciled in Ireland are Low Volatility Net Asset Value (LV-NAV) MMFs. Ireland also serves as a large centre for MMFs denominated in USD and GBP.[6]

|

Chart 7. Growth of MMFs in Ireland |

|

|

Source: Central Bank of Ireland |

MMFs were first established in Ireland in the early 1990s. As many promoters of Irish funds had US backgrounds they wished to establish their MMFs as constant or stable net asset value (NAV) MMFs in order to operate in a similar manner to their US MMFs. In the context of the European UCITS regulatory regime, this meant that there were three important issues to consider:

- where assets were traded (in order to comply with the eligible assets rules in the Directive);

- how assets were to be valued; and

- the use of repurchase agreements.

With regard to valuation, the use of amortised cost methodology was permitted in Ireland by the Central Bank, taking into account regulatory practice that had developed in the US including rules in relation to Weighted Average Maturity and Weighted Average Life. In accordance with the UCITS regime, the rules in relation to valuation were required to be set down in the fund rules. The Central Bank provided certain guidance in relation to the valuation rules for MMFs and this guidance continued to be developed over the years. For example, the Central Bank required MMFs to carry out weekly reviews of the amortised cost valuation versus the market valuation – if there were discrepancies in excess of 0.3 per cent the review was required to move to a daily basis with escalation procedures in place with fund managers and fund boards. Rules in relation to the use of repo (reverse repo in this instance) were also developed by the Central Bank where there were important requirements related to collateral – eligibility, re-investment, and a prohibition on re-use.

Following the global financial crisis in 2008, Ireland was supportive of a European-wide regime for MMFs which was initially achieved with the Committee of European Securities Regulator (CESR) Guidelines “A Common Definition of European MMFs”. The regulatory regime for MMFs underwent further significant change with the implementation of the EU Money Market Fund Regulation (MMFR) which came into effect in 2018. In line with the MMFR, the Commission is required to undertake a review of the Regulation (due by July 2022 but yet to be published).

III. ASSET CLASSES

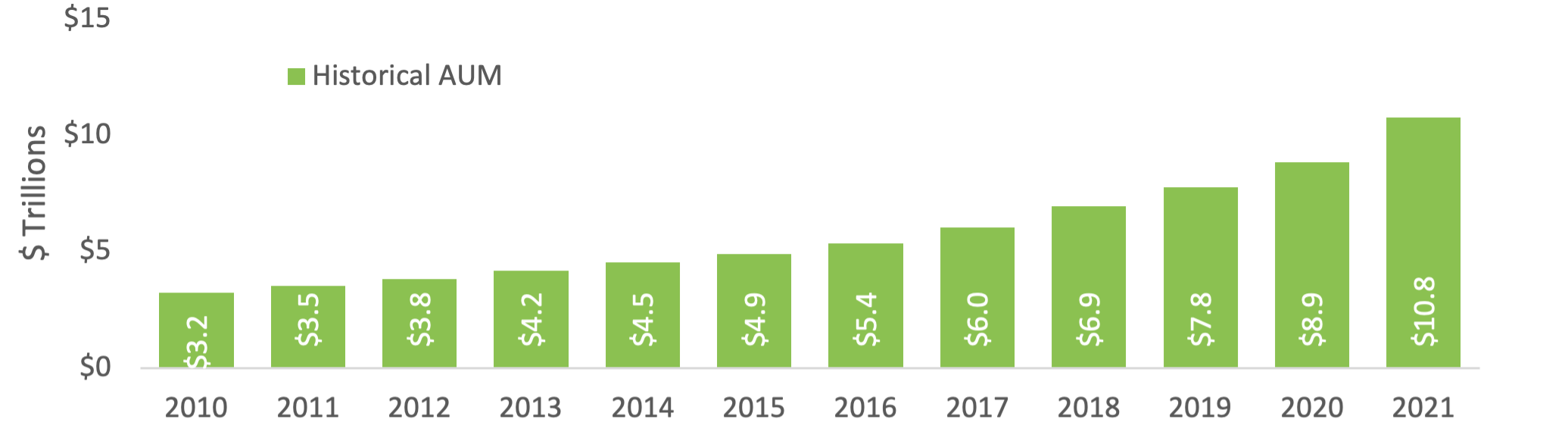

Investment funds invest in a wide range of securities (bonds, equities etc.) with a more recent focus on private assets. There has been significant growth globally in the investment being made in alternative asset classes which include hedge funds, private equity, venture capital, property, direct lending/loan origination, infrastructure and Funds of funds. Investment in private assets (alternative-type investments) are typically illiquid and funds investing in these asset types are usually targeted at professional investors rather than retail investors.

|

Chart 8. Global Growth of Private Capital |

|

|

Source: Pitchbook |

IV. FUND SERVICING AND ADMINISTRATION

There is a diverse range of fund service providers that operate in the funds sector and support the effective functioning of investment. These include firms that must be appointed to the fund such as the fund manager (responsible for all aspects of the management of the fund) and the depositary (responsible for safeguarding the assets of the fund). In addition, there will be other parties such as the fund administrator (may interact with investors and maintain the records of the fund) or an investment manager (responsible for making the investment decisions) that may be appointed by the fund manager. Finally, there are other service providers operating in the sector including legal advisors, accountancy firms and tax advisors as well as Euronext Dublin which is an important funds listing hub.

Ireland is recognised as a centre of excellence in the provision of accounting, administrative and shareholder services to investment funds. This expertise has been built up since the 1990s. This is a result of a specific legal framework being put in place for the activity, alongside an emphasis on the regulation of fund administration in its own right.

Fund administrators have been authorised by the Central Bank under the Investment Intermediaries Act since 1995. The regulation of fund administrators has resulted in certain benefits, including high standards in a critical function that is integral to the good functioning of a fund and providing independence through a separate legal entity. This has increased the attractiveness of Ireland as a funds domicile and as a location for the administration of both Irish and non-Irish investment funds.

V. SUSTAINABLE INVESTING

The EU has undertaken a number of initiatives in the area of sustainability over the last number of years, with Member States working towards the goal of achieving climate-neutrality by 2050. As part of this ambition, the EU as a whole must increase its efforts in order to reach the target of reducing greenhouse gas emissions by at least 55 per cent by 2030. This shift to a more sustainable, low-carbon and circular economy requires significant investment and the funds sector has an important part to play in mobilising private capital.

The growth of the sustainable finance sector has been accompanied by the development of a new EU framework, several aspects of which impact on the funds sector. The Taxonomy Regulation, introduced in July 2020, classifies environmentally sustainable economic activities, while the Sustainable Finance Disclosure Regulation (SFDR) that was introduced in March 2021 sets out mandatory disclosure requirements for funds and other financial products.

These frameworks, along with other EU initiatives, seek to enhance transparency and promote high standards of sustainability and ESG (environmental, social and governance) claims made by financial market participants, as well as protecting investors from risks such as greenwashing. This is an evolving area of work with a particular focus on ensuring investors’ capital is channelled appropriately to sustainable and ESG-related activities and providing investors with reliable data on their investments.

The SFDR classifies funds into three categories indicating their level of sustainability:

|

Table 1. SFDR Categorisation |

||

|

Article 6 – All Funds |

Article 8 – All ESG |

Article 9 - Sustainable |

|

All managed products |

‘Light green’ funds |

‘Dark green’ funds |

|

No integration of sustainability Can include stocks that are excluded from ESG funds, such as tobacco and coal producers, and should be clearly labelled as non-sustainable |

Promotes, among other characteristics, environmental or social characteristics, or a combination but is not a main focus |

“Do no significant harm” |

Source: Department of Finance analysis |

||

According to Morningstar, assets in Article 8 and Article 9 funds across the EU rose by more than 3 per cent in the first quarter of 2023 to €4.9 trillion, pushing their combined market share higher to 57 per cent as a proportion of EU domiciled UCITS (less MMFs).[7] This trend is expected to continue over time in response to strong investor demand for ESG investments.

The role of non-bank financial intermediation

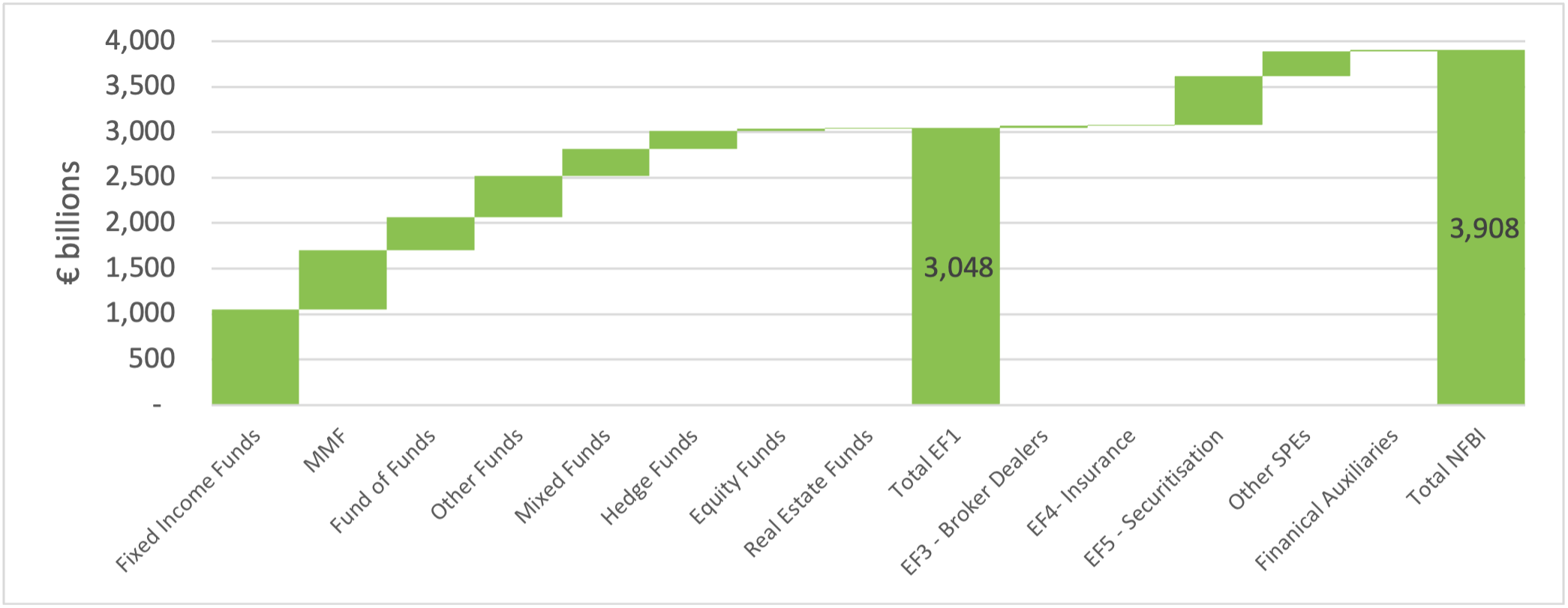

An element of the funds and pensions/insurance sector undertake bank-like activities (“credit intermediation activities”), playing an increasingly important role in financing the real economy and in managing the savings of households and corporates. The Irish non-bank financial intermediation (NBFI) sector grew from €1.24 trillion at the end of 2010 to €3.9 trillion at the end of 2021.

While the NBFI sector in Ireland is broad and diverse, with a variety of business models, much of the growth can be attributed to the investment funds sector which saw its total assets increase to €3 trillion at the end of 2021.

Special Purpose Entities (SPEs), which are not investment funds, are a significant, yet separate aspect of the financial services industry in Ireland. The AUM in SPEs that form part of the NBFI sector is estimated at a further €808 billion as of the end of 2021.

|

Chart 9. Non-bank Financial Intermediation in Ireland at end 2021 |

|

|

Source: Central Bank of Ireland |

As the firms and entity types that make up the NBFI sector are broad and carry out a diverse range of activities, different parts of the sector are subject to varying types of regulatory requirements. For example, certain segments of the sector are subject to monitoring and analysis (via reporting frameworks) but not subject to conduct or prudential regulatory requirements e.g. SPEs. Other parts of the sector, such as investment funds, are subject to detailed and comprehensive regulatory rules. The regulatory framework will also differ depending on whether the entity in question is a product (investment fund) or a firm (fund manager, fund administrator or depositary).

In response to concerns that the NBFI sector could become a source of systemic risk given the overall scale and interconnectedness of the sector (in its widest meaning), there has been growing commentary around mitigating potential financial stability risks with macro-prudential policy in the non-bank financing sector, which includes parts of the funds sector.

Questions

- What policy supports have been most impactful in attracting the funds sector to Ireland and/or the EU in recent decades?

- What characteristics set Ireland apart from other jurisdictions when selecting a fund’s domicile?

- What are the most important trends evident in the sector?

- What are the key risks and challenges for the sector in the medium- to long-term and how can they be managed?

- What are the key opportunities for the sector in the medium- to long-term and how can they be delivered?

- How will technological change and innovation influence the sector’s future development?

- How best can Ireland position itself in the future as a location of choice for EU and international firms?

- How can Ireland best support the growth and development of the market for ESG products and the transition to carbon neutrality?

- For the NBFI sector, those investment funds providing credit intermediation, what are the key opportunities for the sector in the medium- to long-term and how can they be delivered?

- [1] Central Bank of Ireland Follow up on thematic review of fund management companies’ governance, management and effectiveness (2022)

- [2] Central Bank of Ireland Investment Funds Statistics: Q4 2022 (2023)

- [3] The register is available at https://www.esma.europa.eu/document/register-authorised-european-long-term-investment-funds-eltifs

- [4] REGULATION (EU) 2023/606 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 15 March 2023 amending Regulation (EU) 2015/760 as regards the requirements pertaining to the investment policies and operating conditions of European long-term investment funds and the scope of eligible investment assets, the portfolio composition and diversification requirements and the borrowing of cash and other fund rules

- [5] ECB Statistical Data Warehouse

- [6] ESMA Market Report: EU MMF Market 2023 (2023)

- [7] Morningstar SFDR Article 8 and Article 9 Funds: Q1 2023 in Review (2023)